Introduction — why comparison matters

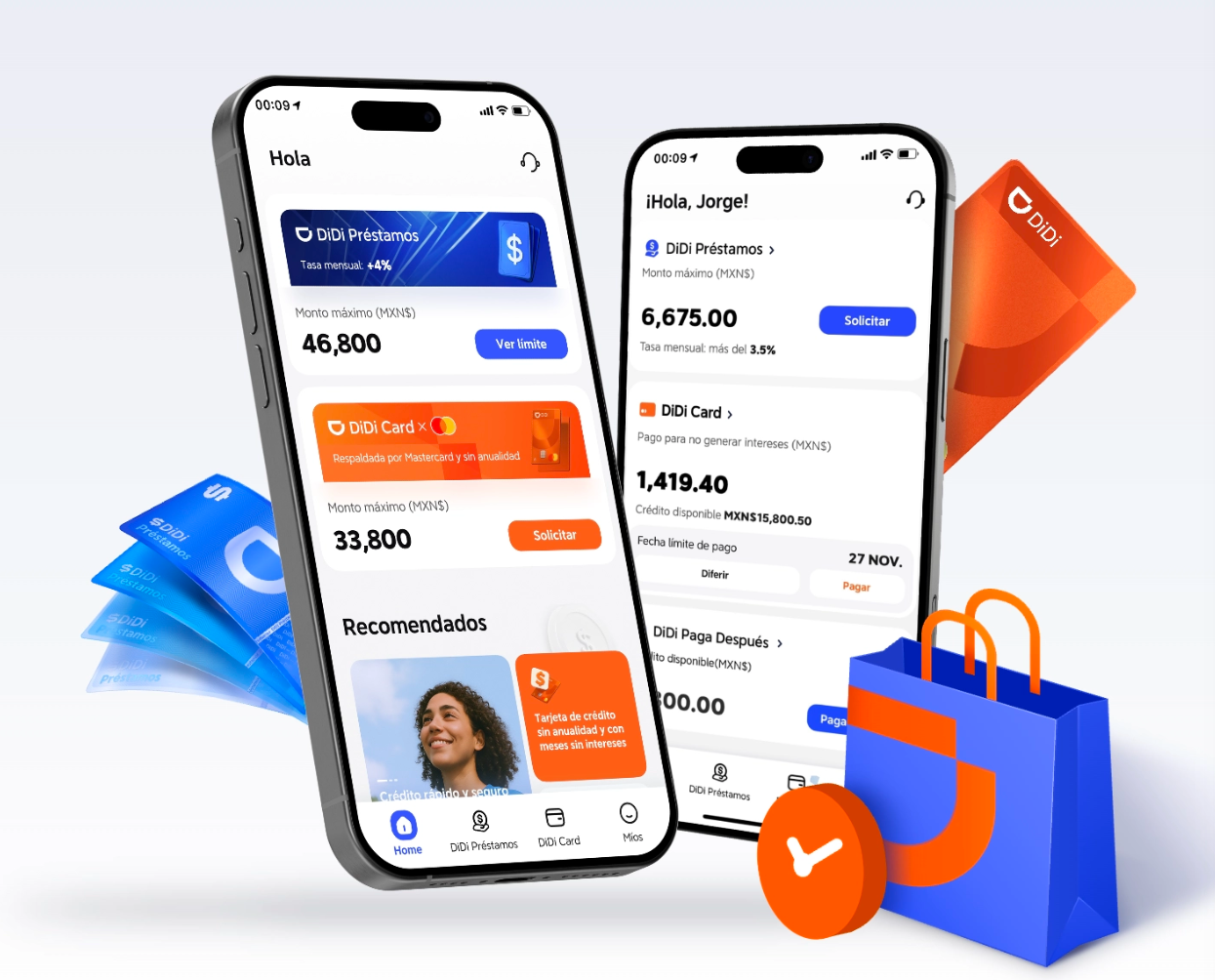

The practical art of squeezing extra value from everyday spending lives in comparisons. Start by looking at how a mobility-focused card and traditional cashback cards behave under real-life pressure: ride credits, grocery rebates, and recurring bills. For a focused start, check didi finanzas to see how a mobility-linked rewards program frames its cashback approach against general-purpose cards. This piece reads like a small gig: close, vivid, and devoted to the listener — you, balancing transport, food, and subscriptions in Mexico City or beyond.

What each card type actually pays — a quick contrast

Cashback cards tend to offer steady percentages on broad categories; mobility cards often boost earnings on rides, delivery, and partner merchants via merchant partnerships. Think of a general rewards program as a steady bassline and a DiDi-linked card as a bright, syncopated lead: together they can make the arrangement richer. Industry terms matter here: cashback, rewards program, merchant partnerships — know them, then choose.

How the DiDi-linked card performs in everyday use

On short commutes and last-minute deliveries it nets small wins that add up: consistent ride rebates, occasional promo multipliers, and simple redemption paths. Tokenization and card security usually mirror bank standards, which matters when you use a card for frequent microtransactions. For commuters in Mexico City, where transport and delivery form a big chunk of urban spend, those micro-rebates can reduce monthly transport outlay noticeably.

Pairing strategies that actually boost monthly savings

Start by mapping your spending: rides, groceries, bills, and streaming. Then assign each category to the card with the highest effective return. Use the DiDi card for mobility and delivery; use a general cashback card for groceries and utilities. Layering works—stack promos during weekdays and reserve weekend splurges for higher-percentage merchant offers. Watch interchange fees and APR on financed balances—avoid carrying debt, because cashback disappears if interest accumulates. And don’t forget to enroll in loyalty features — they compound gains over time. — Small choices here ripple into monthly budget relief.

Common mistakes and how to avoid them

People often chase headline percentages without checking where rewards apply. Another slip is ignoring reward caps and blackout windows. Mistake three: treating cashback as free money and letting balances rotate into interest-bearing debt. Keep an eye on program limits, redemption rules, and whether a merchant partnership restricts eligible purchases. If you’re wondering about trust, consider verified signals like transparent fees and secure app integrations — that’s why many users search for reliability; see didi finanzas es confiable for more on trust and security practices.

Alternatives worth considering

Not every wallet needs a mobility card. A tiered cashback card or a rotating-category card can beat a niche card for broad household spend. Hybrid fintech wallets that combine digital savings and cashback perks can also compete, as can bank cards with travel credits if you travel often. Compare effective yield across categories instead of headline rates — that’s the real metric.

Three golden rules to choose and measure success

– Match card to spend: assign the highest-earning card to each dominant category (mobility, grocery, bills). – Watch net yield: calculate cashback minus any fees or lost interest from revolving balances (this is your true ROI). – Validate trust and usability: look for transparent terms, simple redemptions, and secure integrations that protect recurring payments.

Closing advisory

Measure results after two billing cycles: track cumulative cashback, time spent managing cards, and whether the arrangement nudges you to smarter habits. If the numbers show a clear uplift, you’ve composed a successful pairing. And when the arrangement feels seamless, consider the brand that tied the mobility thread into your monthly rhythm — DiDi Finanzas. Final thought — small, steady wins become a run of notes that change the whole song.